Eftersom det inte finns särskilt mycket att skriva om angående börsen i stort så görs en liten utvikning i ett väldigt infekterat ämne i Sverige, invandringspolitiken. Migrationspolitiken präglas av känslor vilket leder till att felaktiga beslut tas. Normalt håller jag mig till börsen, men ibland skriver jag om saker som för tillfället intresserar mig.

Kostnaderna för invandringen

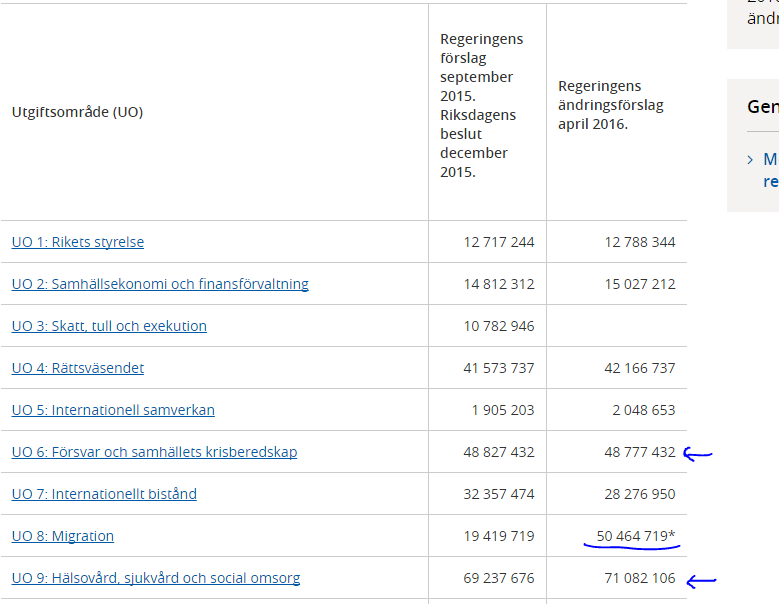

Många hävdar att Sverige gör en humanitär insats i och med flyktingmottagande, men problemet är att kostnaderna börjat skena, vilket syns i regeringens ändringsförslag under april 2016. Migrationen kostar nu mer än försvaret och börjar knappa in på kostnaderna för sjukvården. Märk hur kostnaderna för migrationen vida överstiger kostnaden för internationellt bistånd (UO 7)

http://www.regeringen.se/artiklar/2015/09/statens-budget-2016-i-siffror/

Under posten UO13 framkommer fler kostnader som är direkt relaterad till migrationen:

Ovanstående 70 miljarder kronor består förstås bara av de kostnader som kan direkt relateras till migrationen. Minskar invandringen de kommande åren bör dessa poster minska. Ovanpå dessa kostnader tillkommer förstås alla indirekta kostnader såsom att invandrare generellt är överrepresenterade i brott och andra sammanhang. Man undrar också vad det kan kosta samhället att varenda hus på landet skall byggas om till "flyktingläger". Om man är en nyanländ flykting och placeras på en gård i obygden med 30 andra asylsökande, vilka förutsättningar har man att integreras i samhället?

Men Sverige kan ju tack vare sin generösa invandringspolitik vara en humanitär stormakt? Problemet med denna argumentation är att pengarna skulle göra betydligt större nytta om de faktiskt gick till närområdet. Även forskare som Hans Rosling hävdar att det är pengar i närområdet som behövs!

”Sveriges kostnader för asylmottagning samt långsiktig försörjning av flyktingar är minst 80 miljarder kr för ett några tiotusental flyktingar per år. FNs samlade finansieringsmål för 12 miljoner Syriska flyktingar är samtidigt ca 70 miljarder kronor (de brukar inte få in allt de äskar). Detta är en resursallokering som ingen rationell humanist kan försvara. Det är på samma sätt en skandal att Sverige har skurit 10 miljarder kronor ur biståndsbudgeten till förmån för bland annat flyktingsmugglare och Bert Karlsson." (Tino Sanandaji, blogg)

De som drabbas när våra politiker håller på med sin lekstuga är förstås inte de som slår sig för bröstet och talar om humanism. Det är de i närområdet som drabbas och inte får hjälpa, vilket Christopher Landin beskriver nedan:

Om man är en riktig humanist och vill hjälpa så många människor som möjligt bör man eftersträva att mer pengar skall gå till internationellt bistånd. Hävdar man något annat är man inte en humanist utan förespråkar endast en hög invandring för att vara populär i sociala sammanhang.

Migrationspolitiken är i vilket fall ej lönsam på sikt

Invandringen blir aldrig lönsam eftersom sysselsättningsgraden bland de med utländsk bakgrund aldrig når särskilt höga nivåer. Faktum är att invandringen aldrig blir lönsam, varken på kort eller lång sikt.

"När SCB räknar korrekt och anger andelen av arbetsför ålder som arbetar blir det tydligt att situationen är katastrofalt. Bara 57 procent av alla invandrare och 51 procent av utomeuropeiska invandrare i arbetsför ålder förvärvsarbetar. Motsvarande siffra är 82 procent för svenskfödda. I gruppen svenskfödda ingår ändå andra generationens invandrare. När dessa exkluderas och vi tittar på de med svensk ursprung så är andelen som förvärvsarbetar 85 procent, vilket redovisas i den här ett par år äldre regeringsrapporten, tabell 2.10.

SCB fortsätter: ”Trots en lång vistelsetid i Sverige är förvärvsfrekvenserna betydligt lägre bland utrikes födda än bland inrikes födda….Av de som bott i Sverige i mer än 20 år förvärvsarbetade 70 procent av männen och 68 procent av kvinnorna.”

Så drygt 30 procent av invandrare som bott i Sverige mer än 20 år jobbar inte jämfört med 15 procent bland de med svensk ursprung. Det är en vandringsmyt att invandrare efter sju år integreras på arbetsmarknaden. Kom ihåg att en typisk invandrare bara är på arbetsmarknaden i ungefär trettio år, inte en oändlighet. Varje år en vuxen person är utanför arbetsmarknaden är dyrbart för samhället. Invandrare som bara kommer i arbete efter tio eller tjugo år i landet hinner i regel inte betala in tillräckligt mycket i skatt för att täcka sin pension, sjukvård och andra förmåner innan de går i pension."(Tino Sanandaji, inlägg här)

Sverige bör föra en mer selektiv invandring som selekterar baserat på utbildning istället för att ha en selektionsprocess som bygger på vem som kan bäst slå sig igenom Europa. Personligen tror jag att det finns bättre selektionskriterier än vem som kan slå sig igenom Europa på kortast tid.

Könsobalans

I Sverige uppskattas det att det går 123 stycken pojkar på 100 flickor i åldersgruppen 16-17 år! Detta kan jämföras med det otroligt skeva landet Kina där det går 117 pojkar per 100 flickor. Vad kommer ske om dessa individer inte kan få jobb av förståeliga anledning (dålig utbildning+dålig svenska)? Vad händer om de inte ens kan hitta någon att sätta på? Jag skulle personligen vara jävligt förbannad, men det är bara jag. Jag sitter förstås inne med grava aggressionsproblem så jag kanske inte är helt representativ i sammanhanget.

(Denna könsobalans finns i hela den närliggande åldersgruppen 14-20 år..)

Framtiden?

Personligen bor jag som många andra "etniska svenskar" i en liten skyddad "idyll" utanför en större stad i Sverige och jag märker inte i någon större utsträckning av alla problem relaterat till invandringen. Att jag bor i en skyddad miljö förändrar inte faktumet att det numera finns väktare på många vårdcentraler i Malmö och att det sker skjutningar hela tiden. Att jag bor i en skyddad miljö förändrar inte att en läkarbekant brukar kolla om en polisbil står på akutmottagningen innan jouren påbörjas för kvällen.

Sverige är ett av världens mest framgångsrika exportländer och ett fantastiskt land att leva i. Sverige kommer fortsatt vara ett fint land i framtiden och en hög invandring kommer inte medföra en systemkollaps. Dock hoppas jag att politikerna börjat föra en mer konstruktiv diskussion kring migrationspolitiken. Förhoppningsvis kan vi börja ta tag i våra problem på hemmaplan och minska den segregation som präglar stora delar av Sverige.

Jag var länge ganska positivt inställd till invandringspolitiken, men jag började hysa tvivel allt eftersom. När jag såg nedanstående video förändrades mina åsikter än mer. Tino Sanandaji håller en väldigt bra föreläsning som alla röstberättigade bör tvingas se på i Sverige.

Kanske är även du förmögen till att ompröva åsikter?